![]()

Download the DoctusTech app and start learning today. No credit card required. No expiry.

Start 14-Day HCC DOC Trial

If you are interested in a trial of our HCC Coding Mobile App, please share your information below and we will respond right away.

Calculate Revenue from RAF Scores for your Medicare Advantage Population

In the CMS risk-adjustment model, every patient gets a risk-adjustment factor (RAF) score that determines how much the PCP’s healthcare organization is reimbursed for their care.

In this guide, we’ll discuss how these RAF scores are determined, and how you can use them to calculate revenue from your Medicare Advantage Population.

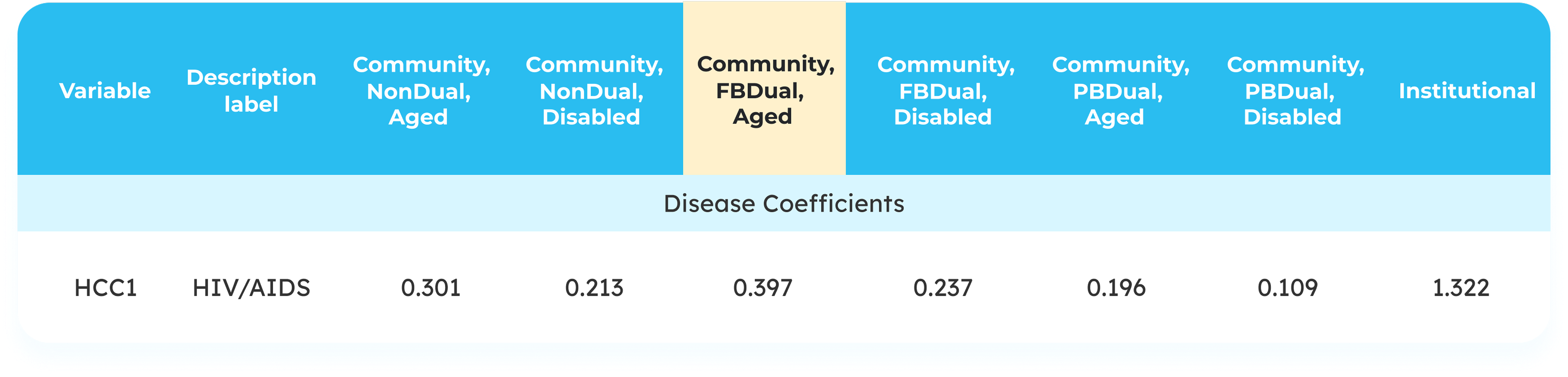

For the purposes of this guide, we’ll be using an imaginary patient as an example: a 72-year-old male, qualified for Medicare before turning 65, is fully dual eligible and has the following V28 HCCs:

- HCC 37: Diabetes with Chronic Complications

- HCC 48: Morbid Obesity

- HCC 155: Major Depression, Moderate or Severe

- HCC 226: Heart Failure

- HCC 238: Specified Heart Arrhythmias

- HCC 254: Monoplegia, Other Paralytic Syndromes

Grouping patients

Almost every variable that goes into the RAF calculation will change based on the patient’s eligibility for Medicare Advantage.

Key Variables include Medicare eligibility category, Medicaid eligibility with Medicare, and Living Situation.

Medicare eligibility category

- Patients who join Medicare Advantage after age 65 fall into one of three ‘Aged’ groupings.

- Patients who join before age 65 are placed into the ‘Disabled’ grouping.

- If a patient originally grouped as ‘Disabled’ turns 65, they are reclassified into an ‘Aged’ grouping but with the RAF modifier ‘Originally Disabled’.

Medicaid Eligibility with Medicare

- Not eligible

- Partially dual eligible

- Fully dual eligible

Living Situation

- Patients living in the community are grouped under Community.

- Patients requiring long-term care are placed in the Institutional grouping.

The table below illustrates how each grouping impacts RAF calculations.

As a 75-year-old, fully dual-eligible male who wasn’t previously grouped as disabled, our example patient will fall into the ‘Community, FBDual, Aged’ column when calculating RAF values.

Step 1: Assign demographic factors

Before a patient even sees their healthcare provider, they’re given a baseline RAF value based on demographic factors including age and sex. Medicare divides patient ages into the following categories:

The example below shows how a patient’s age and sex helps determine their baseline RAF value:

Our patient – a 72-year-old male with dual eligibility – gets a demographic score of 0.626.

Step 2: Assign HCCs

CMS divides ICD-10 codes into hierarchicalcondition categories (HCCs) and assigns each HCC a different value.

Unfortunately, CMS uses a highly-complicated formula to assign RAF values to HCCs – involving complex variables including VA adjustment factors, regional cost differences, and more. Furthermore, this formula, the value of each variable, and even the variables themselves change year-on-year.

Tables such as those found on the CMS website can help you keep track of these annual changes.

For the purposes of our example, we are using the base values as of 12/9/2025.

Once you’ve calculated the patient’s baseline RAF value, it’s time to calculate the RAF value of their HCCs. In our imaginary patient’s case, we get 1.907. Adding that to our demographic score of 0.626, we get a total of 2.533.

Step 3: RAF modifiers

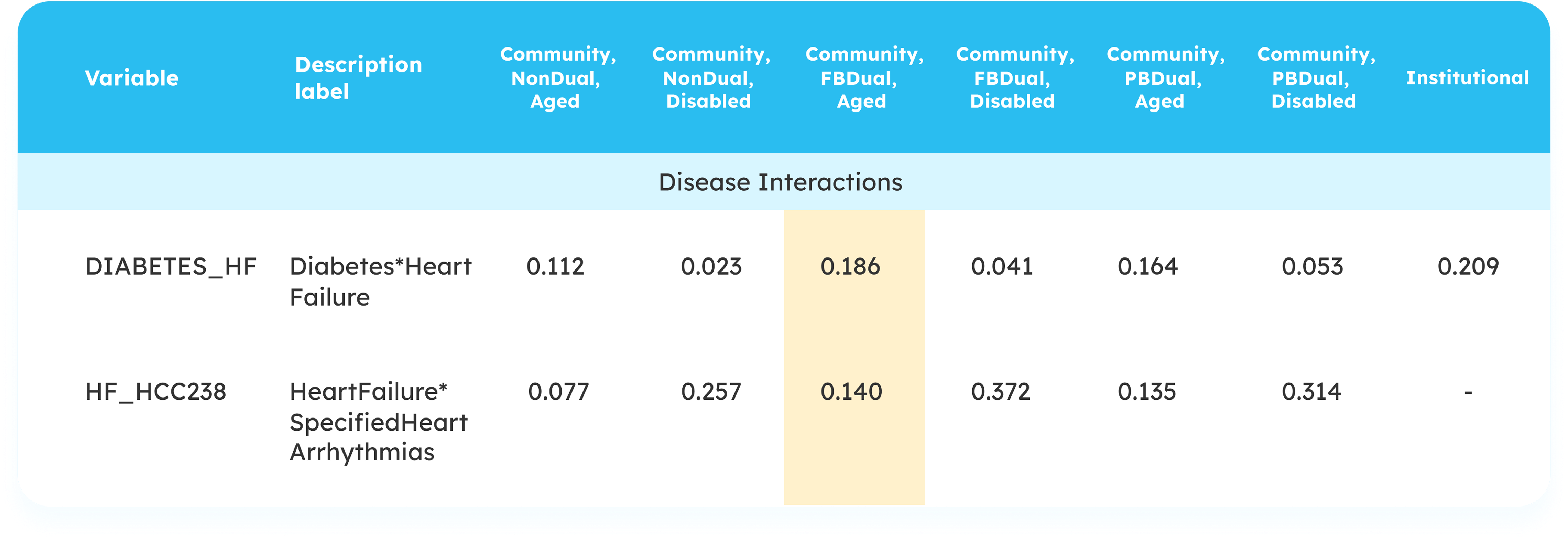

At the end of each year, CMS assesses whether each patient is eligible for the add-on RAF modifiers: the Disease Interaction modifier and the Payment HCC Count modifier. In HCC-V28, six combinations of HCCs are included in the Disease Interaction modifier: for example, heart failure and kidney disease.

The table below shows how such combinations can add to a patient’s RAF score:

Our patient is eligible for two disease interaction modifiers: one for the combination of diabetes and CHF, and the second for CHF and arrhythmias. These modifiers total 0.323, which brings our total to 2.859.

The Payment HCC Count modifier is an additional RAF value added when a clinician has documented a large number of different HCCs on a single patient. The modifier begins at 5 HCCs, with the added value increasing with each new HCC until it caps out at 10.

Our example patient has six HCCs, so he gets an additional 0.071 added to his RAF score. That brings our total raw RAF to 2.930.

Step 4: CMS backend adjustments

At this point, the RAF total is known as the “raw risk score”. This score undergoes two final alterations before the number is finalized:

- The normalization factor. Each year, a new normalization ratio is determined by examining five years of patient data from a variety of locations. From this data, an average patient profile and risk score is generated. CMS then takes this score and multiplies it by whatever number is required to make the RAF 1.0.

This multiplier then becomes the normalization factor and is applied to every patient’s raw risk score. For example, the normalization factor for 2025 is 1.045 raw risk scores will be divided by this number to keep the baseline RAF at 1.0. - MA coding adjustment is a percentage decrease designed to compensate for the difference in coding practices between risk-adjustment and fee-for-service coders. This figure has remained consistent at 5.9% for some time and is not expected to change in the near future.

Once these adjustments have been applied, you have your final RAF score. Let’s run these numbers for our imaginary patient.

Our patient’s raw RAF score is 2.930. We divide that by the normalization factor of 1.045 to get 2.804.

Lastly, the MA coding adjustment factor is subtracted from this normalized’ RAF score. Remember, this figure is a consistent 5.9%.

5.9% of 2.804 = 0.165

2.804 – 0.165 = 2.639

This number is our final RAF score. To calculate the revenue from this patient, we simply multiply this RAF score by the 2025 base rate of $10,402.34.

2.639 x $10,402.34 = $27,451.78

This figure represents the total revenue for this particular Medicare Advantage patient. By repeating this process for each patient in your MA population, you get the total revenue.